Netting interest on overpayments against subsequent interest due is allowed in certain tax jurisdictions. California’s “Avon” rule, for example, allows such interest netting. The calculation of interest netting is easily accommodated by Instant Interest.

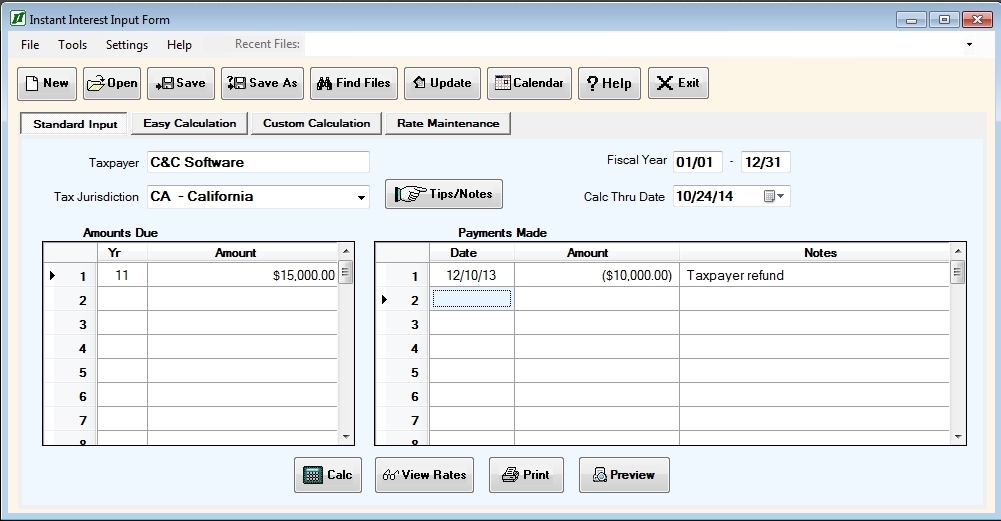

For example, suppose a taxpayer requests a refund of $10,000 on a 2011 return. The state has 90 days to refund the principal without being required to pay interest. The state generated the refund on 12/10/13 and pays it to the taxpayer. On October 24, 2014, per audit, the state assesses the taxpayer $25,000 for the 2011 tax return which was due on 03/15/12. Interest is calculated on $15,000 from 03/15/12 to 12/10/13 and $25,000 from 12/10/13 to 10/24/14.

To duplicate the state’s calculation, enter $15,000 in the “Amounts Due” column for the 2011 year. Under the “Amounts Paid” column you would enter a credit amount of (10,000) with the date 12/10/13.

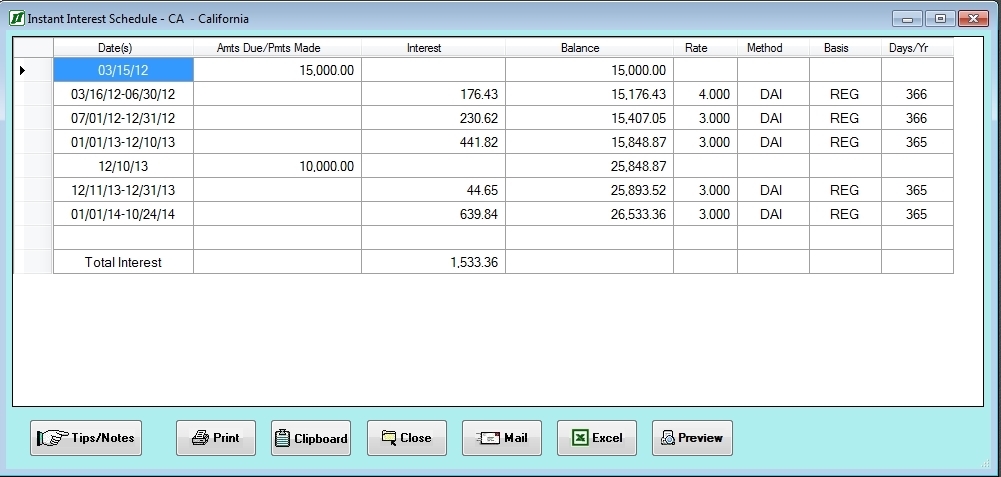

The program treats credit or negative amounts in the “Payments Made” column as additional amounts due or as an assessment, resulting in the following calculation.

You would only apply this netting once, and future assessments or federal Revenue Agent Report (RAR) payments would calculate the entire amount from the due date of the return.