Some tax jurisdictions have begun to charge an additional 2 points added to the standard interest rates for large underpayments (in excess of $100,000) if the amount due is not paid within 30 days of notification. This is generally known as “hot interest.” The jurisdictions with “hot interest” rules are:

Jurisdiction Law in Effect Beginning CA – California 01/01/92 FED – Federal 01/01/91 VA – Virginia 01/01/91

When you calculate interest and these conditions are satisfied, Instant Interest will display the following prompt:

For Federal underpayments, the notification date is defined under the revisions to Section 6621 of the IRS Code enacted through the Revenue Reconciliation Act of 1990 as the earlier of:

“(i) the date on which the 1st letter of proposed deficiency which allows the taxpayer an opportunity for administrative review in the Internal Revenue Service Office of Appeals is sent, or

(ii) the date on which the deficiency notice under section 6212 is sent.”

The amended language also states that “in the case of any underpayment of any tax imposed by this subtitle to which the deficiency procedures do not apply, subparagraph (A) shall be applied by taking into account any letter or notice provided by the Secretary which notifies the taxpayer of the assessment or proposed assessment of the tax.” The two states follow this same general approach.

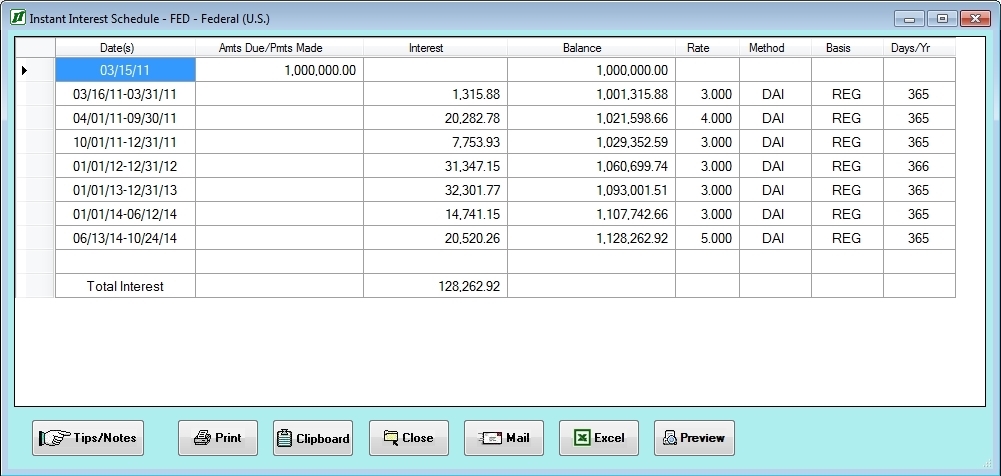

Instant Interest calculates a date 30 days after the Deficiency Notification Date. For the time after either this date or the date designated in the law governing underpayments, whichever is later, Instant Interest will add 2% to the normal interest rate for underpayments. If the deficiency is for a tax period from January 1, 1985, through December 31, 1988, Instant Interest will first prompt you for whether or not to treat the transaction as a tax-motivated transaction and then for the Deficiency Notification Date. When the interest schedule is displayed or printed, an additional date will be inserted into the schedule to reflect the date at which the additional 2% began.

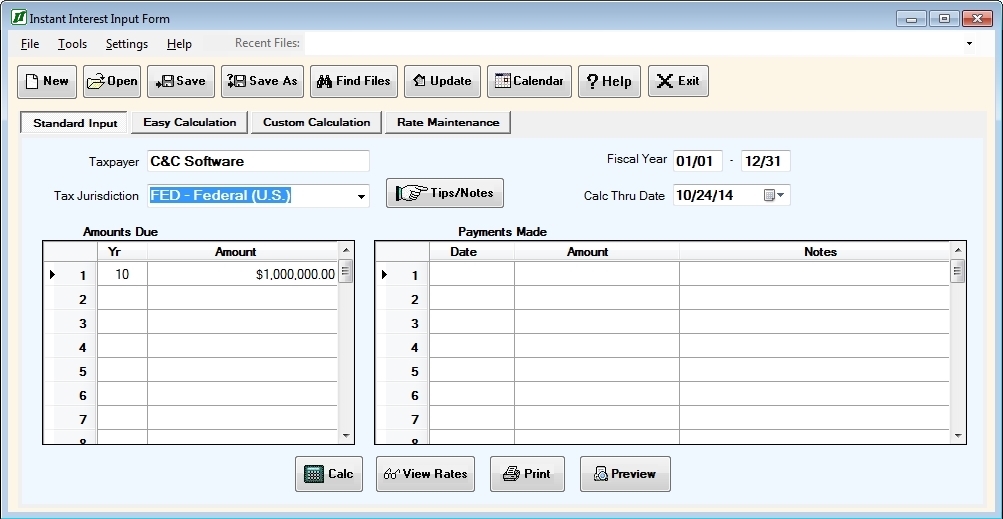

For example, suppose you are calculating a deficiency through 10/24/14 on an amount of $1,000,000 for fiscal year 2010, and you were notified of that on May 13, 2014. First you would enter:

When you are prompted for a notification date you would enter:

The resulting calculation would look like this:

Because this type of transaction changes the interest rate in use, you should not mix large and “non-large” payments on the same interest schedule as they should be calculated using different rates. Instant Interest uses the amount for the earliest fiscal year being calculated to determine whether or not a schedule is to be calculated as a large underpayment.