"Restricted interest" relates to special provisions in the law which limit or prohibit interest under certain conditions which the law stipulates. In general, interest is paid on a tax overpayment for the time the government has the use of the taxpayer’s money. Similarly, interest is collected for the time the taxpayer has use of the government’s money. The underlying objective is to determine in a given situation whose money it is and for how long the other party had the use of it. (Rev. Proc. 60-17). Although income tax may be reduced by a carryback such as a net operating loss, net capital loss, investment credit, or a work incentive program credit the computation of interest is not affected by the carryback until the "filing day of the taxable year in which the loss or credit arises" – Proposed Reg 301.6601-1(e). (For returns and refunds filed before October 3, 1982, the interest computation is not affected until the last day of the taxable year in which the credit or loss arose). The interest application of foreign taxes which are carried back is under dispute with the IRS under the Fluor Corporation case currently in the U.S. Court of Federal Claims.

Instant Interest can help you calculate the interest due in these and other "what if" scenarios. We recommend, however, you consult with a competent tax advisor to determine the timing and proper application of restricted interest.

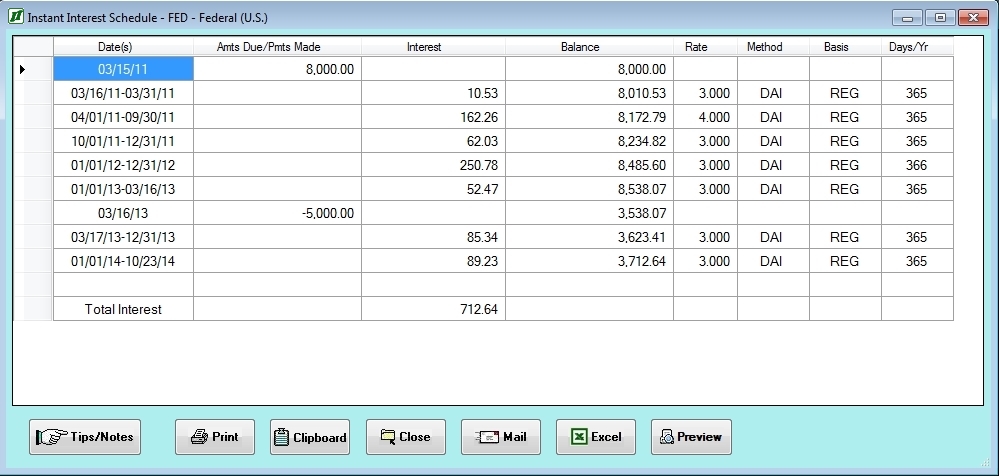

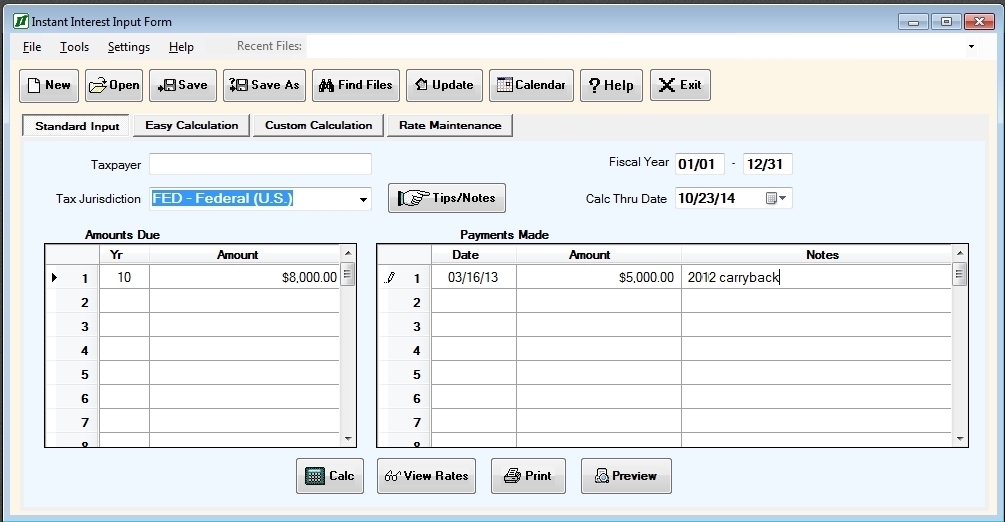

To see how the calculation works, suppose a credit carryback from 2010 in the amount of $5,000 reduces your $8,000 tax liability for 2012 to $3,000. You plan to pay the additional liability on October 23, 2014. Interest, however, is computed by the IRS on the 2010 amount of $8,000 before the carryback until the due date of the 2012 tax return — March 15, 2013 (calendar year taxpayer). You would enter the $8,000 in the Amounts Due column for 2010 and $5,000 with a date of 3/16/13 in the Payments Made table, as follows:

Instant Interest will calculate the amount of interest to October 23, 2014, as follows: