Before 10/11/93, Utah used the over/ underpayment interest rate that was in effect at the time the tax was due without regard to any subsequent changes in the legislated interest rate. The same is true of New York City before 02/24/83.

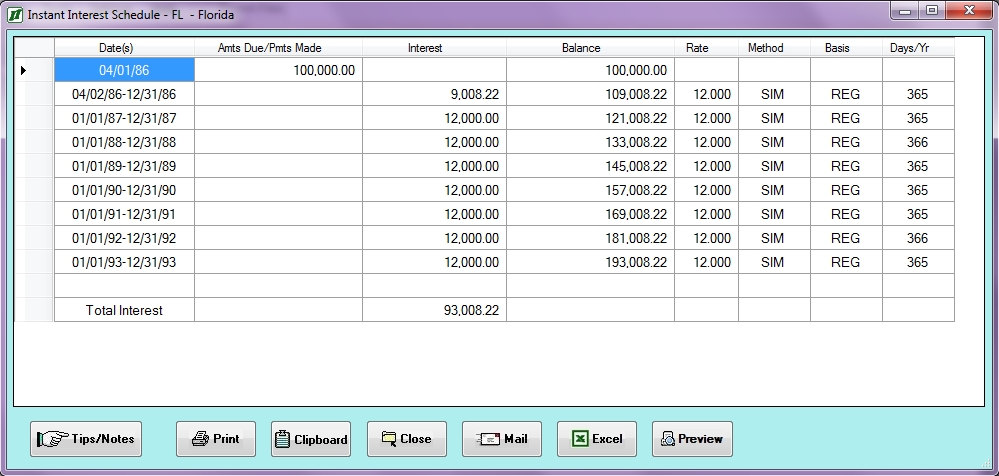

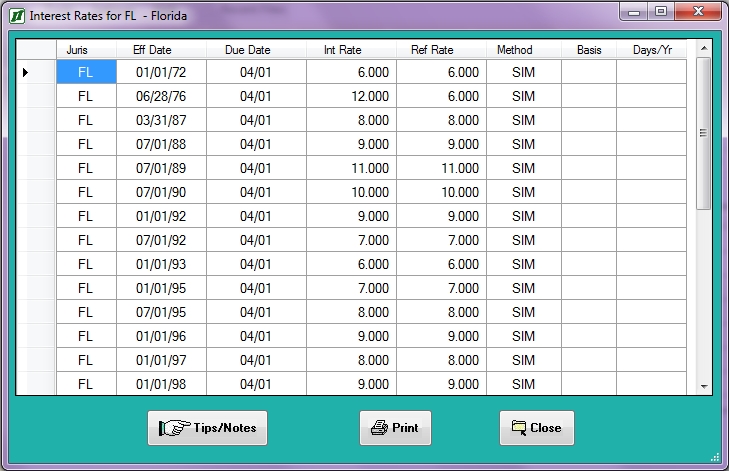

Beginning 06/28/76 Florida used a flat 12% interest rate for underpayments on any taxes regardless of any subsequent legislated rate changes. This law continued in effect until 04/01/87 (the due date for taxes due 12/31/86). For example, although the rate screen for Florida may appear as follows:

an interest schedule for an underpayment of $100,000 due 04/01/85 calculated through 03/31/06 would appear as follows: